This 3 bed 1 bath ranch home is situated on 3 acres of land in desirable Pittsgrove Township New Jersey. Everything on one floor for easy living. This home offers a living room with a barn slider that opens up to a large family room with vaulted ceilings and so much natural light . The floor plan provides a layout that’s flows seamlessly and is comfortable for everyday living. Spacious kitchen opens up to the dining area that offers plenty of room for family meals or entertaining. Dining room offers sliders to the back screen porch where you can enjoy sitting and overlooking the serene nature. The owner has updated the flooring and hot water heater.

Enjoy grilling with the family out on the large deck or walking the land, this home has so much to offer. Current owner has lots chickens and sheep. Full basement with inside entrance, provides extra space for storage, hobbies and the laundry area. Home includes plenty of parking, beautiful outdoor space, and chicken coups that can be left for the next family. Give us a call to make this home yours today.

Stacy Schnell

D: 856-364-0772

Salesperson Collini Real Estate

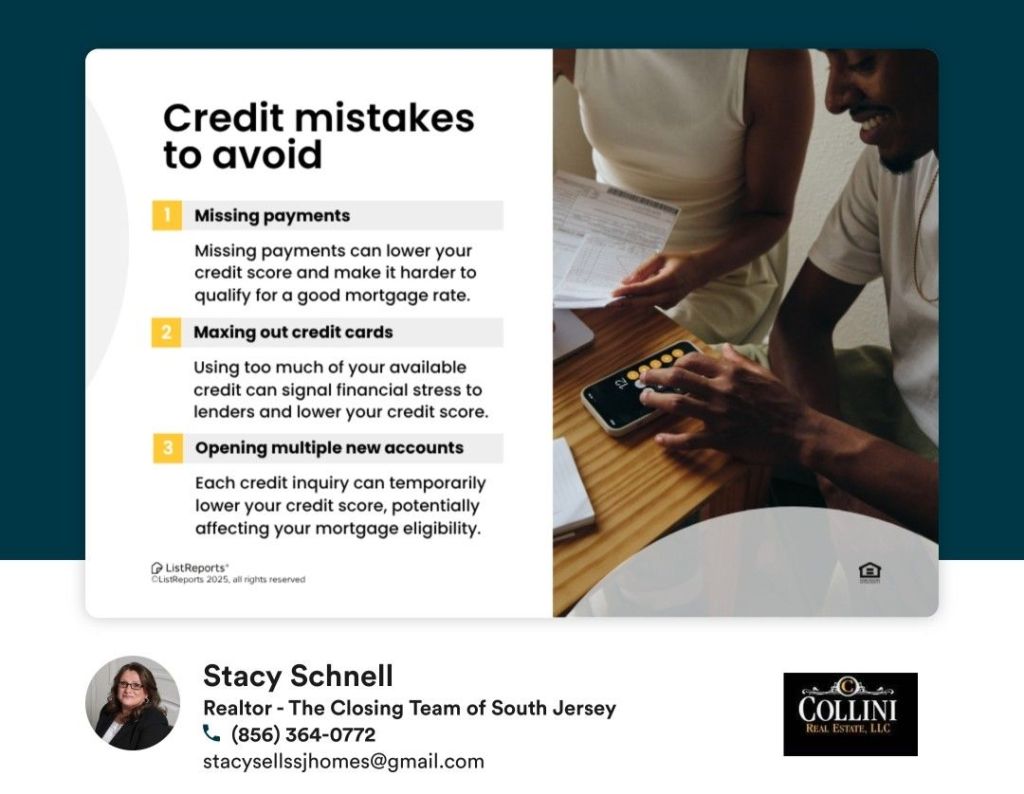

Subscribe to get access to the rest of this post and other subscriber-only content.

Current rates in New Jersey are 4.081% for a 30-year fixed, 3.587% for a 15-year fixed, and 4.017% for a 5/1 adjustable-rate mortgage (ARM).

Mortgage Rates See Biggest One-Week Drop in a Decade. Mortgage rates fell more in the past week than they have in any one-week period in more than a decade. The average 30-year fixed loan has dropped 22 basis points to 4.06%, while 15-year fixed loans are down 14 basis points to 3.57%, according to Freddie Mac.Mar 28, 2019

Compare today’s average mortgage rates in the state of New Jersey. Bankrate aggregates mortgage rates from multiple sources to provide averages for New Jersey.

To Read more CLICK HERE

Below is a link with a few handy tips for first time home buyers.

The most important thing you can do is hire a full time professional to help guide you throught the process. Please feel free to give me a call anytime. Whether buying your first home, 2nd home or making an investment I would be happy to assist.

Stacy Schnell 856-364-0772

An FHA loan is a mortgage that’s insured by the Federal Housing Administration (FHA). They are popular especially among first time home buyers because they allow down payments of 3.5% for credit scores of 580+. However, borrowers must pay mortgage insurance premiums, which protects the lender if a borrower defaults.

Borrowers can qualify for an FHA loan with a down payment as little as 3.5% for a credit score of 580 or higher. The borrower’s credit score can be between 500 – 579 if a 10% down payment is made. It’s important to remember though, that the lower the credit score, the higher the interest borrowers will receive.

The FHA program was created in response to the rash of foreclosures and defaults that happened in 1930s; to provide mortgage lenders with adequate insurance; and to help stimulate the housing market by making loans accessible and affordable for people with less than stellar credit or a low down payment. Essentially, the federal government insures loans for FHA-approved lenders in order to reduce their risk of loss if a borrower defaults on their mortgage payments.

For borrowers interested in buying a home with an FHA loan with the low down payment amount of 3.5%, applicants must have a minimum FICO score of 580 to qualify. However, having a credit score that’s lower than 580 doesn’t necessarily exclude you from FHA loan eligibility. You just need to have a minimum down payment of 10%.

The credit score and down payment amounts are just two of the requirements of FHA loans. Here’s a complete list of FHA loan requirements, which are set by the Federal Housing Authority:

Typically an FHA loan is one of the easiest types of mortgage loans to qualify for because it requires a lowdown payment and you can have less-than-perfect credit. For FHA loans, down payment of 3.5 percent is required for maximum financing. Borrowers with credit scores as low as 500 can qualify for an FHA loan.

Borrowers who cannot afford a 20 percent down payment, have a lower credit score, or can’t get approved for private mortgage insurance should look into whether an FHA loan is the best option for their personal scenario.

Another advantage of an FHA loan it is an assumable mortgage which means if you want to sell your home, the buyer can “assume” the loan you have. People who have low or bad credit, have undergone a bankruptcy or have been foreclosed upon may be able to still qualify for an FHA loan.

You knew there had to be a catch, and here it is: Because an FHA loan does not have the strict standards of a conventional loan, it requires two kinds of mortgage insurance premiums: one is paid in full upfront -– or, it can be financed into the mortgage –- and the other is a monthly payment. Also, FHA loans require that the house meet certain conditions and must be appraised by an FHA-approved appraiser.

Upfront mortgage insurance premium (UFMIP) — Appropriately named, this is a one-time upfront monthly premium payment, which means borrowers will pay a premium of 1.75% of the home loan, regardless of their credit score. Example: $300,000 loan x 1.75% = $5,250. This sum can be paid upfront at closing as part of the settlement charges or can be rolled into the mortgage.

This excerpt from Zillow to Read more on how to qualify simply CLICK HERE