This 3 bed 1 bath ranch home is situated on 3 acres of land in desirable Pittsgrove Township New Jersey. Everything on one floor for easy living. This home offers a living room with a barn slider that opens up to a large family room with vaulted ceilings and so much natural light . The floor plan provides a layout that’s flows seamlessly and is comfortable for everyday living. Spacious kitchen opens up to the dining area that offers plenty of room for family meals or entertaining. Dining room offers sliders to the back screen porch where you can enjoy sitting and overlooking the serene nature. The owner has updated the flooring and hot water heater.

Enjoy grilling with the family out on the large deck or walking the land, this home has so much to offer. Current owner has lots chickens and sheep. Full basement with inside entrance, provides extra space for storage, hobbies and the laundry area. Home includes plenty of parking, beautiful outdoor space, and chicken coups that can be left for the next family. Give us a call to make this home yours today.

Stacy Schnell

D: 856-364-0772

Salesperson Collini Real Estate

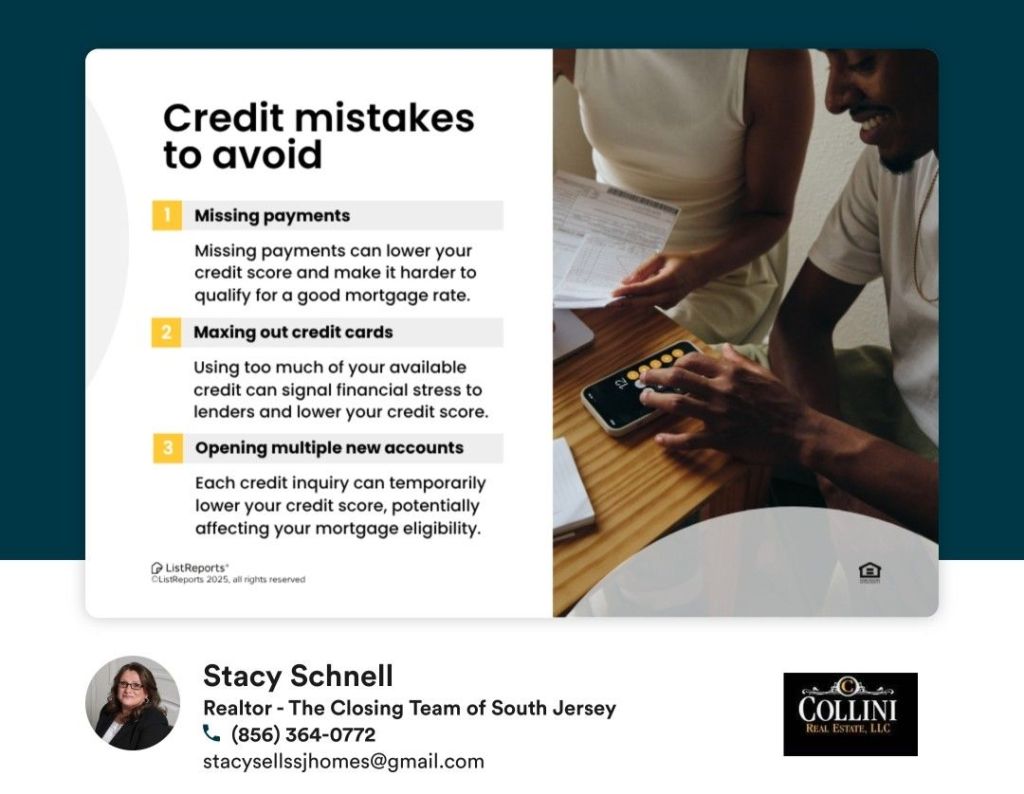

Subscribe to get access to the rest of this post and other subscriber-only content.

Current rates in New Jersey are 4.081% for a 30-year fixed, 3.587% for a 15-year fixed, and 4.017% for a 5/1 adjustable-rate mortgage (ARM).

Mortgage Rates See Biggest One-Week Drop in a Decade. Mortgage rates fell more in the past week than they have in any one-week period in more than a decade. The average 30-year fixed loan has dropped 22 basis points to 4.06%, while 15-year fixed loans are down 14 basis points to 3.57%, according to Freddie Mac.Mar 28, 2019

Compare today’s average mortgage rates in the state of New Jersey. Bankrate aggregates mortgage rates from multiple sources to provide averages for New Jersey.

To Read more CLICK HERE

Featuring 4 bedrooma and 3 Baths. This 2 story home is situated on quiet lot on cul-de-sac street in Millville, New Jersey. Completely updated kitchen has wood countertops, new stainless steel appliances, backsplash, freshly painted cabinets, breakfast nook, pantry closet, ceiling fan and double sink with garbage disposal. Kitchen opens up to dining area with a floor to ceiling stone wood burning fireplace and ceiling fan. Separate laundry room and family room off kitchen. Spacious and remodeled foyer entry with exposed wood walls and new flooring. Large master bedroom has cathedral ceilings, ceiling fan and a walk-in closet. Master bath has a double vanity, stall shower, soaking tub and tile flooring. Other features include a partially finished basement, insulated windows, natural gas heat with humidifier, central air, concrete driveway, rear deck, city water and sewer and a large rear yard with two sheds. Solar panels are leased and offer a great savings on your electric bill. Rieck Avenue elementary school. Convenient access to Routes 49, 47 and 55. This listing is presented by The Scott Sheppard Team. Call today for a tour or more information and ask about property #90. Or for more information about homes for sale in Cumberland County. Ask about our new $0 down FHA loans! Stacy Schnell ~ Realtor Associate Cell: 856-364-0772

Listed for just $148,000. This bungalow features a completely upgraded kitchen, maple cabinets with soft-close drawers, granite countertops, tile backsplash, tile flooring and recessed lighting. Kitchen opens to dining room and living room with bamboo floors. Living room has a gas fireplace and ceiling fan. Full basement with bilco doors, walk up attic with attic fan. Roof 6 years old, replacement windows, security system, covered front porch, rear maintenance free deck, fenced yard, driveway parking with carport in rear of home, shed. Natural gas heat and hot water, central air condenser 1 year old, public water and sewer, Mt. Pleasant Elementary School. Easily accesible to Routes 49 and 55. This property is presented by The Scott Sheppard Team. Give us a call to schedule your private tour today! Ask about home # 89. Stacy Schnell ~ Realtor Associate Cell: 856-364-0772

Though you may be willing to spend a certain amount, the real determination of how much house you can afford is driven by how much a lender calculates you can afford. So before you begin to search for the perfect house, it is very important to begin the homebuying process by getting preapproved. Getting preapproved for a home mortgage loan will provide you with a preliminary statement on the size of loan for which you can qualify. Knowing this, you can then focus your home search.

In general, lenders allow your total monthly housing costs to go as high as but not more than 30 percent of your gross monthly income. The second requirement is that not more than 36 percent of your gross monthly income can be tied up in the total monthly house payment and payments on long-term debt.

Visit my Website to read more and for adiitional information about obtaining a mortgage. Please feel free to give a call anytime for assistance with the home buying process!

Stacy Schnell – Realtor Associate – Cell: 856-364-0772

Qualifying for a Federal Housing Administration (FHA) loan can be much easier compared with a conventional one. Borrowers will need a valid Social Security number, and be a lawful resident of legal age to be able to sign an FHA loan. Qualifying for a loan requires a minimum credit score of 500 in addition to a FHA-approved property appraisal and a favorable debt-to-income ratio.

This excerpt from Valuepenguin.com Click HERE to read more.

Visit my website stacyschnell.com for more helpful information on getting prepared to purchase a home or call me anytime, Id be happy to assist!

Stacy Schnell – Realtor Associate Cell: 856-364-0772